Small cap stocks are renowned for rewarding investors with huge returns – a stellar stock can double, quadruple, or rise 10-fold in value over a short time.

Software company Pro Medicus has risen more than 200 times from 50¢ per share in 2013 to $105 this week, which means an investment of $5000 has turned into $1 million, while shares in buy-now-pay later group Afterpay raced from their $1 initial public offer price in 2016 to more than $150 in 2021.

The life-changing capital gains on offer attract many amateur investors looking to back winners, but the sector is also notorious for capital losses; success stories are rare among the thousands of companies that bite the dust.

The significant risk means small and micro cap investing is as much about avoiding the losers as identifying the winners, says Marcus Burns, the co-founder and portfolio manager of Spheria Asset Management.

“If a company doesn’t have earnings or sales it’s 99 per cent likely to be a disaster for you,” he says. “There are lots of stocks talked to the moon by brokers and management teams, but normally, it’s just hot air.”

Marcus Burns, portfolio manager at Spheria Asset Management. Louie Douvis

Marcus Burns, portfolio manager at Spheria Asset Management. Louie Douvis

Roughly 75 per cent of all companies open to public shareholders are “unhealthy”, the ASX 2023 Australian Investor Study found.

A micro cap is generally defined as a company with market capitalisation of less than $30 million and a small cap less than $1 billion. Companies that are listed (as opposed to privately owned) are required to disclose their financial accounts to the ASX on a quarterly or semi-annual basis.

Small caps both here and overseas have failed to keep up with the rally in larger caps over the past few years, but some analysts are tipping a resurgence. This is because once interest rates start coming down, as many suggest will happen later this year, borrowing costs will ease. Small companies tend to find it harder to raise capital so have to rely on borrowing.

The standard benchmark for professional small-cap investors is the S&P/ASX Small Ordinaries Index, which has returned a combined capital gain of 13 per cent over the past five years.

Now though, a pivot by global central banks to cut interest rates may push more money into small-cap stocks as the S&P/ASX Small Ordinaries Index outperformed its large-cap benchmark for two consecutive quarters for the first time since 2021.

Institutional investors are also interested. The $206 billion Future Fund signalled its conviction for a revival when last year it appointed Sydney-based money manager Maple-Brown Abbott to run a small-cap segment as part of a wider return to active stock picking.

The majority of small and micro cap losers come from the mining sector, where founders are desperate to raise money for speculative exploration. Technology, biotech and industrial small-caps (companies involved in the construction, manufacturing, and defence industries) are also statistically likely to lose investors money.

At least half-a-dozen companies in the buy-now-pay-later space lost more than 90 per cent of their value, or filed for bankruptcy over the past few years including Zip Co, Zebit, Beforepay, Openpay, Laybuy and Splitit to wreck the returns of speculators.

Burns says the number-one rule for small cap stock pickers is to focus on the business fundamentals of growing profits and sales. Typically, small cap investors want a track record of five years of profitability from a company, depending on how much risk they’re prepared to take.

After ensuring a business is profitable, make sure it has a strong balance sheet, Burns says. That means little to no debt with cash on hand. Such information can be garnered from the accounts of public companies available on the ASX’s website.

Three things to look for

“There are three ways to make a return on small stocks: dividend yield, earnings per share growth or [profit] multiple expansion,” says Richard Ivers, a portfolio manager with Prime Value Asset Management. “That gives you a framework for how to find companies.”

Dividend yield shows how much a company pays investors in dividends as a percentage of its stock price. The higher the yield based on past payments the more income an investor should receive. However, high yield going forward is never guaranteed, as any company can run into trouble and cancel or lower dividends.

Richard Ivers likes funeral operator Propel Funerals. Louis Trerise

Richard Ivers likes funeral operator Propel Funerals. Louis Trerise

Earnings per share growth shows how quickly a company is growing profits per share and is usually expressed in percentage terms. If a company earns $10 per share in 2023 and $12 per share in 2024, its earnings per share growth is 20 per cent.

The third of Ivers’ tips is profit multiple expansion, which occurs when investors become more optimistic about a stock’s prospects.

“Dividend yield in small caps is typically not big, so you should focus on earnings growth and valuation multiples,” Ivers says. “But just because something is growing doesn’t mean it’s valuable. You’ve also got to look at duration of earnings. A toll road business with decades of earnings is slow growth, but much more valuable than something that might just be growing quickly.”

Ivers names funeral operator Propel Funerals as a business that has grown slowly and consistently over a long time. “Over the last four years earnings have gone from 15¢ per share to 20¢ per share, and the PE [price-to-earnings] multiple has gone up from 18 times to 29 times, so the stock has doubled with about a third of it from the EPS growth and the rest from the PE multiple expansion,” he says.

Ivers also identifies financial services business Equity Trustees and insurance broker Austbrokers as small businesses boasting the operational and financial qualities to make them decent bets for capital growth.

Greg Suefong, a senior financial adviser at Financial Spectrum, warns that owning small caps makes investors more susceptible to swinging with general economic conditions and market sentiment.

“If you have a well-diversified portfolio of small caps, you’re not likely to suffer a total capital loss, so you can allocate part of your portfolio to these,” he says.

How much you allocate to small caps depends on your situation, including how much you have to invest and your income requirements, Suefong says.

“If you have a large portfolio and your income needs are covered with your current assets, you could put anything up to 15 per cent into small caps,” he says. “If, however, you are drawing down on capital regularly to meet your income needs [retirees are a prime example], then no more than 5 per cent would be appropriate. You can invest more if you’re a high risk-taker, but statistically, only about 1 per cent of the population would fit this category.”

Return on capital and net profit

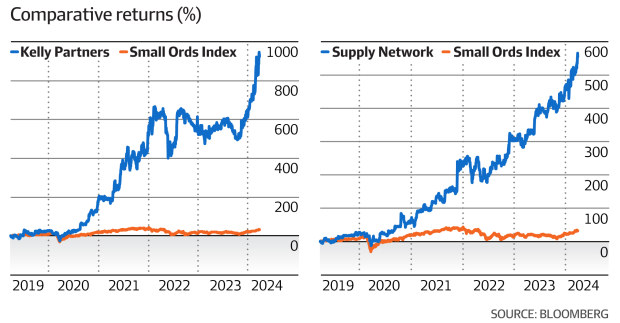

One under-the-radar small-cap business Burns likes is truck and bus parts business Supply Networks, with the stock rocketing more than 400 per cent over five years.

“Supply Networks has grown revenue by 12 per cent plus for the last 10 years and earnings by 15 per cent-plus,” Burns says. “The return on capital has gone from 25 to 50 per cent, so it has expanded [its profitability] as it has been growing. It’s actually a Google-type business, as it can reinvest capital for growth and has grown its share price faster than Google.”

Return on capital is another key metric for investors to consider in that it shows how much additional growth a business can deliver by reinvesting profits into its operations.

Broker MA Financial backed Burns’ view on Supply Networks and rated it a buy with a $21.26 price target, versus a market price of $18.30. MA Financial’s analysts also said they liked the stock as it had grown net profit at a compound rate of 27 per cent between financial 2018 to financial 2023.

Net profit is another important indicator of potential success because owning shares in a company entitles to you a share of net profit. If it grows over time so should the value of your shares.

Karen Towle, small cap fund manager with Tribeca Group. Louie Douvis

Karen Towle, small cap fund manager with Tribeca Group. Louie Douvis

Karen Towle, a micro cap stock picker for the Tribeca Special Opportunities Strategy Fund, says smaller businesses are outperforming their larger and more defensive rivals after February’s profit reporting season showed fears over an economic slowdown in Australia in 2024 are overblown.

Even though mining and industrials are notoriously difficult to get right, Towle likes Genus Plus and Spartan.

Genus Plus provides building services for the telco and electricity industries, tapping the energy transition theme.

“The big opportunity for them in the eastern states is increasing demand for electricity usage,” Towle says. “It’s really well-placed to help develop the gird and it’s a very well-run, family-owned business.”

Towle also likes West Australian gold driller Spartan as the metal’s price raced to a record high of $US2285 an ounce on Wednesday.

“It’s drilling a site called Never, Never in WA. It’s an extremely high-grade deposit and in production it should be one of the highest margin gold plays in WA. Tribeca is also still constructive on the gold price and our view is that Spartan is also a potential takeover target.”

Network and flywheel effects

Josh Clark, a portfolio manager and small cap stock picker at QVG Capital, says sustainability is critical to small cap investing and this is demonstrated by a track record of earnings growth.

“If you’re going to pay a [profit] multiple for a business you want to be damn sure those earnings will be there going forward,” he says. “That’s even more true in small caps as markets will punish them more than large caps if things go wrong.”

Clark says the best small caps will also show signs of competitive advantages that allow them to grow profits faster than rivals.

“A competitive advantage may be a network effect, or scale where you can grow profits faster than sales, or economies shared with customers that creates a flywheel effect,” he says. “But all small caps have got some hairs, there’s no such thing as a perfect one.”

The network effect is the idea that the value of a product or service increases as more people use it. Uber and Lyft, for example, are able to provide better service to riders when more drivers join the platform.

The flywheel effect can be summarised as business growth delivering more success. For example, as online retailer Amazon has gained scale, it has been able to cut prices and therefore attract more customers.

Founder-led

Clark’s QVG Capital has backed software businesses like Xero and Hansen Technologies in the past as they’re “capital light”, which means they can grow profits with minimal reinvestment required into the business.

Dean Fergie, the co-founder of Cyan Investment Management and a 25-year veteran of picking small stocks on the ASX, says many investors fail to make sure a business has a sufficiently strong balance sheet.

“Don’t buy businesses operating on a promise,” he says. “These concept stocks can go really well, but you’ve got to appreciate the risk you’re taking as your downside is significant. You’re investing in hype and hoping for good news, rather than buying on fundamentals.”

Many small-cap businesses may boast they’re developing disruptive technology or medical treatments, but commonly it turns out those types of loose promises amount to nothing.

Fergie says a basic indicator that a company may be aligned to investors – rather than selling them a story – is where a founder retains a significant shareholding in a business that is growing profits and sales. Information about ownership interests in a public company is available in its annual report.

“Brett Kelly at [accounting roll-up] Kelly Partners Group is 50 per cent owner and executive chairman, he runs it like his own business and is really good at what he does,” Fergie says. Kelly Partners shares are up 748 per cent over the past five years and closed at $6.87 on Wednesday.